Why haven't growth and inflation slowed more?

Why haven't growth and inflation slowed more?

It is not in the interest of the Elites

The world’s central banks raced at an extraordinary pace over the past year to cool inflation, but it hasn’t proved enough—yet.

Economic growth remains mostly solid and price pressures strong across affluent countries despite sharply higher interest rates.

Why haven’t growth and inflation slowed more? Much of the explanation lies in the pandemic’s weird effects and the time it takes for central-bank rate increases to curb economic activity. Additionally, historically tight labor markets have fueled wage gains and consumer spending. [WSJ]

There hasn’t been a central banker who understood how to stop inflation since Paul Volcker. (The Fed Funds Rate peaked at 19.08 January 1981) A lengthier explanation of The Volcker Cure can be seen in the following:

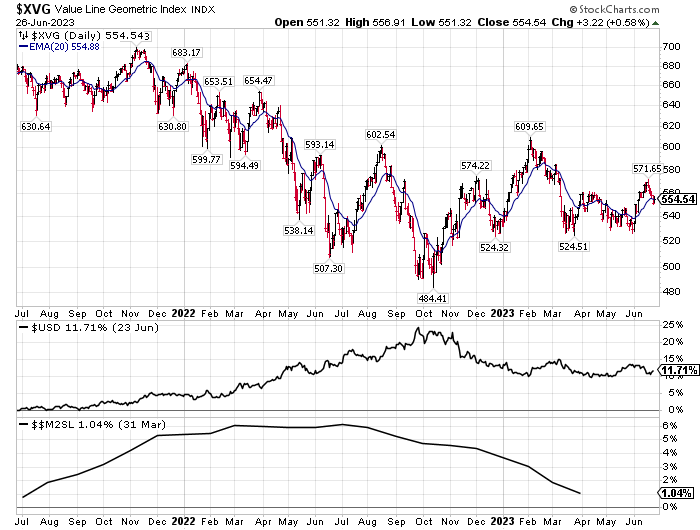

At any rate, no central banker of recent memory has really tried to quell inflation; rather, they are consumed with preserving their own sinecures through politically acceptable Band-Aids. The following graph of the events leading up to the Sub-Prime Mortgage crash illustrates what must take place for the Real Economy to “get back to normal”.

The dollar must fall. Note that the Dollar began to decline (relative to a basket of currencies) in 2006. Notice, too, that the money stock (M2) climbed throughout that time. Central bankers blather on about the tools available for quelling inflation, but at its core lies one fact: the purchasing power of a dollar held at any moment in time must be reduced for excess demand to be diminished.

How are we doing today? Since the dawn of COVID, the Fed has committed anywhere from $5 to $7 trillion funding the Hunger Games of the Sovereign—none of which goes to producing goods and services on Main Street. Increased demand (all that new cash) meets a shrinking supply, and what do we get? Inflation.

Since 2009, the TMS (True Money Supply) “is now up by nearly 189 percent”.

Out of the current money supply of $19.2 trillion, $4.8 trillion of that has been created since January 2020—or 25 percent. Since 2009, $12.5 trillion of the current money supply has been created. In other words, nearly two-thirds of the money supply have been created over the past thirteen years.

The fact that the money supply is shrinking at all is so remarkable because the money supply almost never gets smaller. The money supply has now fallen by $2.6 trillion (or 12.0 percent) since the peak in April 2022. Proportionally, the drop in money supply since 2022 is the largest fall we’ve seen since the Great Depression. (The money supply fell by 12 percent from its peak of $73 billion in mid-1929 to $64 billion at the end of 1932.)

In spite of this recent drop in total money supply, the trend in money-supply remains well above what existed during the twenty-year period from 1989 to 2009. To return to this trend, the money supply would have to drop at least another $4 trillion or so—or 22 percent—down to a total below $15 trillion.

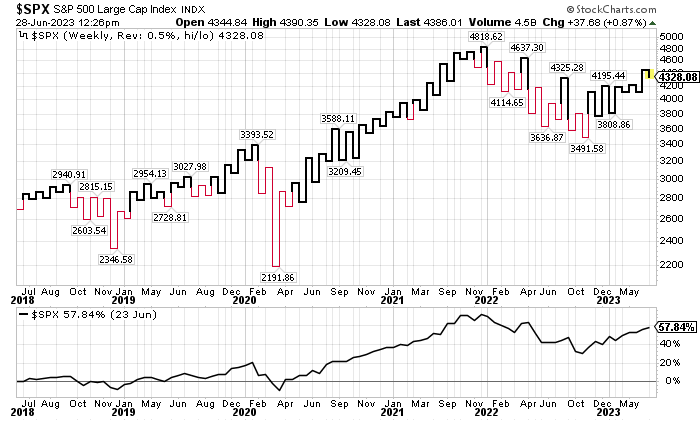

The graph below illustrates what has happened to the dollar in the last two years. (Not shown on the graph is that M2 has jumped since April; hence, the “revitalization” in the economy—or, more realistically, in AI stocks.)

Where did all those newly-minted dollars go before they filtered down to Main Street? This era’s bubble could be called the “Big-Cap Bubble”, as much of the newly-minted dollars were used for stock buybacks and dividends. “Since 1997, share repurchases have surpassed cash dividends and become the dominant form of corporate payout in the U.S.” Since then, trillions of dollars have moved through Wall Street, issuing shares, buying them back, leveraging bets through derivatives, waking up every morning reading Fed tea leaves.

The bubble looks like this:

Two economies?

Two economies exist … in parallel. Most people live in the Real Economy, where goods and services are produced and exchanged, where individuals meet face-to-face, where all the wealth is created. In fact, the fundamental event is the moment of exchange at which time a value is established for the items exchanged. In modern societies, money is the tool by which the value of the exchange is maintained (Unit of Account and Store of Value functions). Otherwise, money also facilitates the exchange by reducing transaction costs (Medium of Exchange function). All wealth is produced in the Real Economy. We know this because of the functions of money. That is in fact why money came into being in the first place.

The inhabitants of the Money Economy are Central Bankers and their elite clients: Heads of State, Barons of Industry, Countries with nuclear weapons. At the core of their existence is money, not to facilitate exchange but to shuffle pieces around on stock-market chess boards, to purchase bling (from yachts to nuclear weapons), and—most important of all—to buy affection from blocs of voters for whom their has been discovered some slight in need of governmental remediation (or at least to avoid another Tiananmen).

The Two Economies exist in parallel linked only by the wormhole of money. The problem is that money serves different purposes in each economic system but is maintained in only one. Sound money is absolutely necessary for the Real Economy to function efficiently. (Interest Rates should tell us the price of accepting a certain risk.) In the Money Economy, cash is a plaything, a chip on the Craps table, a token of one’s place in the hierarchy.

Since at least 1971 when President Nixon ended dollar convertibility to gold, the goal of the federal government has been to enhance the dominion of regulatory agencies over activities in the Real Economy. The pattern has been: discover a problem, pass a law, create an agency to oversee the gears and levers of the activity. The hitch is that when it comes time to budget for this new agency, there is no money. That is where the Federal Reserve steps in to play the part for which it was always intended: funding expansion of the Regulatory Realm.

If the Republican House of Representatives does not “right the ship of state” through the “Power of the Purse”, the greatest experiment in the history of mankind will be lost to the ages. What a pity.