Past is Prologue

Past is Prologue

Those who do not learn from history are doomed to repeat it

[Subprime Mortgage Crash, $HGX = Housing Index]

The Great Recession (2007-2009) has rekindled academic interest in the causes of the ups-and-downs of the business cycle. The earliest models explored whether exogenous (“out-of-the-blue”) shocks could have an effect on output, consumption, investment, and hours. Absent from these models were the effects of monetary policy.

Second generation models looked at the effect of “sticky” prices and wages (Keynes theory that wages/prices rise easily, but are “sticky-down”) as the culprit in causing inflation, followed by a contraction in the economy. [1]

Modern Monetary Theory has taken Keynes to new heights of delirium: politicians no longer need worry about printing fiat currency, helter-skelter. Yet, a recent book suggests that academics have yet to ask the crucial question. Is the business cycle a product of deliberate governmental action?

The book is Boom and Bust. [2]

In 1694, at the age of 22, a Scottish court sentenced [John Law] to death for killing a man in a duel, but he escaped prison and fled to the Continent, growing rich through a combination of professional gambling, financial services and networking.

[T]he famous Harvard economist Joseph Schumpeter placed him ‘in the front rank of monetary theorists of all times’. [3]

Schumpeter studied economics under the tutelage of the forebears of the “Austrian School” of economics. His magnum opus, Capitalism, Socialism, and Democracy, contained a chapter—all of six pages—titled “The Process of Creative Destruction”. So, why would Schumpeter esteem John Law so highly? John Law solved the eternal problem of sovereigns: how to expand the money supply without “clipping coins”.

In 1715, John Law moved to Paris whereupon he “met with the Regent to propose the establishment of a ‘General Bank’ as a branch of government”. But Law’s vision for the General Bank was to have the kingdom’s monetary authority hold “all of the king’s revenues, issuing in their place bank notes that were exchangeable for coins. Once the bank was established, it only needed to hold coins worth a fraction of the value of all outstanding bank notes…. The government could then increase the money supply by lowering the fraction of bank notes backed with coins” [3].

But John Law wasn’t finished. He also concocted “a scheme for the reduction of the public debt”. The Regent had granted Law with a charter “to develop land near the Mississippi River”. And when shares of the Mississippi Company were offered to the public, the only acceptable form of payment was government bonds. “…Even if debt holders noticed that they were getting a raw deal in terms of future cash flows, the prospect of spectacular capital gains on the shares in the short run would be likely to prove too tempting to resist…. In short, Law solved the government’s debt problem by inventing the bubble”. [4]

The Fed’s dual mandate requires it to ensure both stable prices and maximum employment. The traditional tool the Fed uses to accomplish these goals is the adjustment of the federal funds rate, the short-term interest rate that determines how much it costs for banks to lend to each other overnight. The 2007-2008 financial crisis, however, demonstrated that even lowering the interest rate to zero was considered insufficient to shore up economies in freefall, and the Fed turned to more unusual tactics. One of these measures was what the Fed refers to as “large-scale asset purchases,” which is more commonly known as “quantitative easing.” Under this process, the Fed enters the market to buy securities, typically mortgage-backed securities (MBS) and Treasuries, injecting both capital and liquidity into the market. This approach is not without risks – for the first time in its history, the Fed is regulator, supervisor, and now participant in the economy.

As of February 9, the Fed’s assets stand at $8.9 trillion. [5]

The technological change that preceded the Crash of 1929 was the extension of Henry Ford’s method of “mass production” into all manner of manufacturing—and the explosion of credit to pay for it all. The consequence of the crash was to collapse consumer spending, leading to the Great Depression.

The core of all business cycles is the tug-of-war between the greed of the sovereign and the creativity of the entrepreneur. Every sovereign understands that capital-creation is necessary if they are to keep other covetous sovereigns at bay. On the other hand, buying loyalty is never a small enterprise. At least since the Great Depression, American politicians have found it necessary to violate the Constitution in order to maintain their demands on the wealth created by Capitalists. And so it was with the Subprime Bubble.

Unlike so many other bubbles…this one involved not just another commodity but a building block of community and social life and a cornerstone of the economy: the family home. [6]

[T]he securitisation of mortgages created highly marketable instruments which allowed investors from around the globe to speculate billions of dollars on homes in the United States, Spain and the UK. [7]

But there cannot be a bubble unless the availability of money and credit is expanded, and this was done in spades. “Economies such as China, Japan and Germany…recycled the earnings from their exports by sending large amounts of capital to the likes of Ireland, Spain, the United States and the United Kingdom”. Furthermore, the “Federal Reserve kept interest rates low after the dot-com bust and 2001 recession in order to stimulate the economy by encouraging housing starts and home sales with low mortgage rates”. [8]

[B]anks and mortgage lenders substantially reduced their lending standards.

Homes had become marketable objects of speculation and the banking system was supplying seemingly unlimited amounts of leverage to potential speculators. [9]

The theme of Boom and Bust centers on the necessary elements for a Bubble to occur. The authors call these elements The Bubble Triangle. [10]

The starting point of our metaphor is to think of a financial bubble as a fire….

The first side of our bubble triangle, the oxygen for the boom, is marketability: the ease with which an asset can be freely bought and sold.

The fuel for the bubble is money and credit. A bubble can form only when the public has sufficient capital to invest in the asset…. First, the bubble assets themselves may be purchased with borrowed money…. Second, low interest rates on traditionally safe assets, such as government debt or bank deposits, can push investors to ‘reach for yield’ by investing in risky assets instead.

The third side of our bubble triangle, analogous to heat, is speculation…. Once a bubble is under way, professional speculators may purchase an asset they know to be overpriced, planning to re-sell the asset to ‘a greater fool’ to make a capital gain. this practice is commonly referred to as ‘riding the bubble’. [11]

John Law’s Mississippi Bubble came into being because Law was given control of the General Bank: He was in a position to “direct France’s entire monetary policy towards generating the bubble”. [12]

With all three sides of the bubble triangle in place, the emergence of a bubble only required a spark: an initial burst of price increases that could kick off the self-perpetuating process of speculation. This was provided…through a combination of propaganda, the temporary restriction of supply, and commitments to buy shares at prices above market value. Once early purchasers of shares had experienced spectacular capital gains, such measures became less necessary…. But once the fire had spread beyond a certain level, it became impossible to control. [13]

When the Mississippi Bubble went bust, “the price level in Paris fell by 38 percent in 1721, a more severe deflation than the United States experienced during the Great Depression”’ [14]

The Subprime Bubble had its origins in the Clinton and Bush administrations. By this time, politicians had become well connected with Wall Street financiers, who well knew how to facilitate the three sides of the Bubble Triangle.

A bubble is not possible without the fuel of money and credit…. In the case of the United States, it was estimated that just over 60 per cent of the increase in mortgage funds can be directly attributed to this money flowing in from overseas.

However, some economists…have suggested that loose monetary policy and low central bank interest rates were more of a problem…. The Federal Reserve kept interest rates low after the dot-com bust and 2001 recession in order to stimulate the economy by encouraging housing starts and home sales with low mortgage rates. In one sense this worked too well, because low interest rates prompted US consumers to buy houses in an unprecedented fashion.

Low interest rates, however, would not have been such a problem had they not been accompanied by such a dramatic extension of mortgage credit…. In the United States, mortgage debt climbed from $5.3 trillion in 2001 to $10.5 trillion in 2007 and mortgage debt per household rose from $91,500 in 2001 to $149,500 in 2007. To put this in context, mortgage debt in the United States rose almost as much in 6 years as it had in the period from 1776 to 2000!

How was such a large increase in mortgage debt possible? …[B]anks and mortgage lenders substantially reduced their lending standards. The simplest way of doing this was to relax the down payment constraint on mortgages—the loan-to-value ratio…. In the case of the United States, the subprime sector grew from 7.6 percent of mortgage originations in 2001 to 23.5 percent in 2006.

Homes had become marketable objects of speculation and the banking system was supplying seemingly unlimited amounts of leverage to potential speculators.

Wealth inequality had grown inexorably since the 1970s, as the economic gains of globalisation bypassed the lower classes of society. …politicians needed the votes of those who had seen their incomes and prospects stagnate…. Ireland, Spain, the United Kingdom and the United States [used] housing policy to encourage the bottom-income quintiles to buy houses, while incentivising the financial sector to lend to these quintiles. In all four countries, this strategy was adopted by the main parties of both the left and right wing.

[T]he 1977 Community Reinvestment Act (CRA), which had been moribund, became a key part of the drive for affordable housing…. [T]here were commitments of about $3.5 trillion dollars of CRA lending between 1993 and 2007. [15]

The financial engineering of the Subprime Bubble reached new heights via the securitization of mortgages. “This involved a bank ‘distributing’ the mortgages which it had originated by selling their associated cash flows. These cash flows were then sliced, diced and packaged into mortgage-backed securities (MBS): financial assets which entitled the holder to the repayments from a set of underlying mortgages.” [16]

The MBSs were a hit as they offered higher interest rates than did government securities. And rating agencies adorned even the riskiest offerings with AAA crowns.

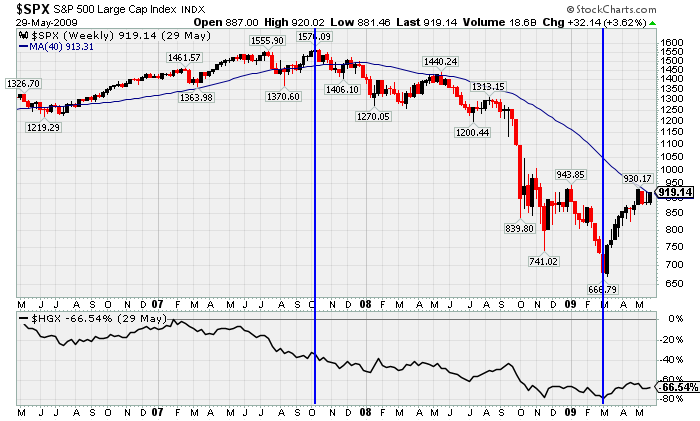

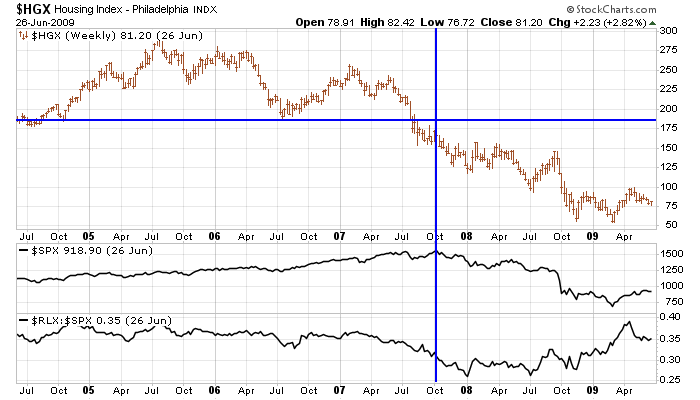

The following chart displays the Housing Index ($HGX) through the Subprime Mortgage Crash. Housing peaked two years (July 2005) before the S&P 500 ($SPX). The ratio of the S&P Retail Index ($RLX) to $SPX peaked at about the same time as $HGX. The Vertical Line indicates the peak of $SPX; the Horizontal Line, a Support Level.

Five investment banks had liabilities of $4 trillion. Lehman Brothers filed bankruptcy. Bear Stearns and Merrill Lynch were taken over by other financial concerns. Goldman Sachs and Morgan Stanley were bailed out. Fannie Mae and Freddie Mac owed $5 trillion in mortgage obligations and were placed in receivership. Eventually, more than100 banks failed. Yet, the well-connected came out smelling like a rose, and the rest of us picked up the tab.

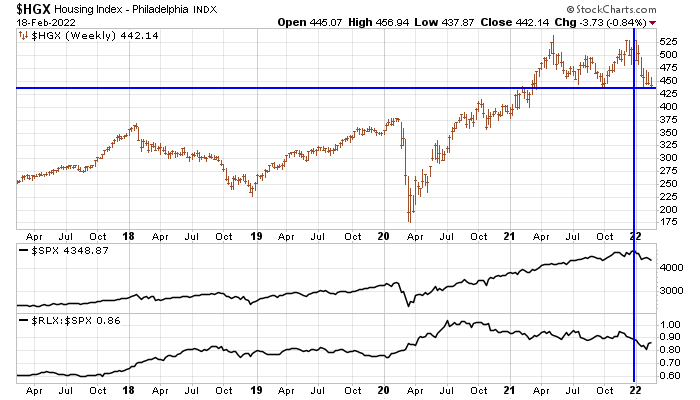

All of the ingredients present in the Subprime Bubble are present in the Wall Street Bubble of today. But the money is going…where? The $trillions that have been appropriated in the name of COVID therapeutics seem to have disappeared into various socialist maws. Will this market go bust? Almost certainly.

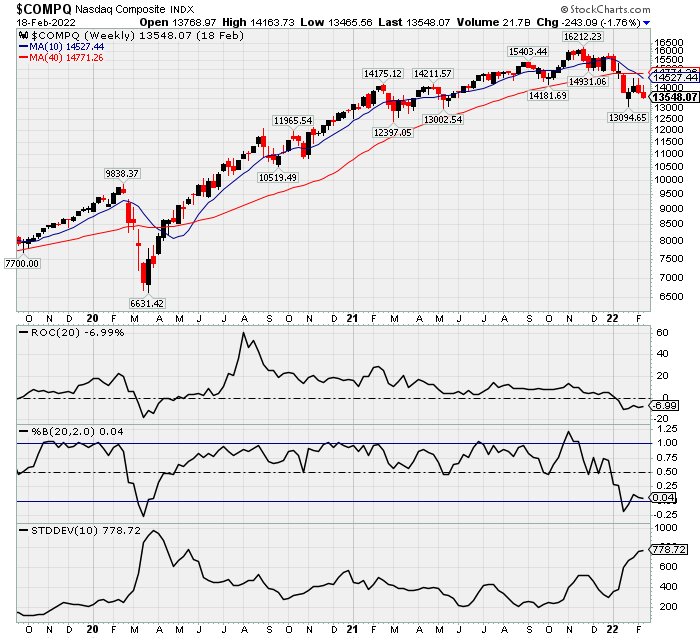

Sector Rotation is a theory that holds that certain market sectors will decline months before the business cycle enters the “Early Recession” phase. The Nasdaq is an index heavily weighted in tech stocks, health care, and consumer discretionary stocks—early indicators of recessionary pressure. Technical Analysts become wary when they see a “Death Cross”—when the 50-day moving average crosses below the 200-day moving average—like what occurred a week ago.

Does anyone care?

As to whether any economics professors will take up the cause, don’t hold your breath. It is unlikely that many economics professors will join in the search for business-cycle methodologies that incorporate deliberate political provocation as the key variable, as practically all universities have been co-opted through grants (from not only the federal government, but also the CCP) and the money-laundering scheme known as “student loan” programs.

NOTES

[1] Kehoe, P. J., Midrigan, V., and Pastorino, E. (Summer 2018). Evolution of modern business cycle models: Accounting for the Great Recession. Journal of Economic Perspectives, Vol. 32, No. 3. (pp. 141-166)

[2] Quinn, W. and Turner, J. D. (2020). Boom and bust: A global history of financial bubbles. Cambridge University Press.

[3] ibid., p.18

[4] ibid., pp.19-20

[5] Wade, T. (February 15, 2022) Tracker: The Federal Reserves’ balance sheet assets. American Action Forum

[6] The Financial Crisis Inquiry Commission, as quoted in Quinn, W. and Turner, J. D. (2020), p. 170

[7] Quinn, W. and Turner, J. D. (2020), p.181

[8] ibid., p. 182

[9] ibid., p. 183

[10] ibid., p. 4

[11] ibid., pp. 4-7

[12] ibid., p. 32

[13] ibid., p. 33

[14] ibid., p. 35

[15] ibid., pp. 182-187

[16] ibid., p. 176